What is NPS?

National Pension System (NPS) is a voluntary, defined contribution retirement savings system. The scheme was introduced in Jan 2014 for the new government employees. NPS is mandatory for all central government employees along with some State government employees who’ve joined after Jan 2004. All can invest in NPS from May 2009.

The main objective of the system is to develop a habit of saving for retirement.

The scheme falls under the jurisdiction of the Pension Fund Regulatory and Development Authority (PFRDA). The aim of NPS is to provide monetary benefits in the form of a pension after an individual reaches retirement.

Eligibility Criteria

- Entry age 18 years to 70 years.

- Person must be Resident Indian, Non-Resident Indian (NRI), or Overseas Citizen of India (OCI).

- Provide valid KYC documents like PAN Card, Address Proof and Aadhar Card etc along with NPS application.

If you meet all the above criteria, you are eligible to open both the NPS Tier 1 Pension Account & NPS Tier 2 Investment Account.

Unicque Selling Proposition of NPS (USP)

NPS is a low-cost product. NPS Tier 1 Pension Account is also providing tax benefits. You are free to choose various asset classes like Equity, Government Bond, Corporate Bond, and Alternate Asset class for investment. You can decide the proportion of asset class as per your risk-taking ability.

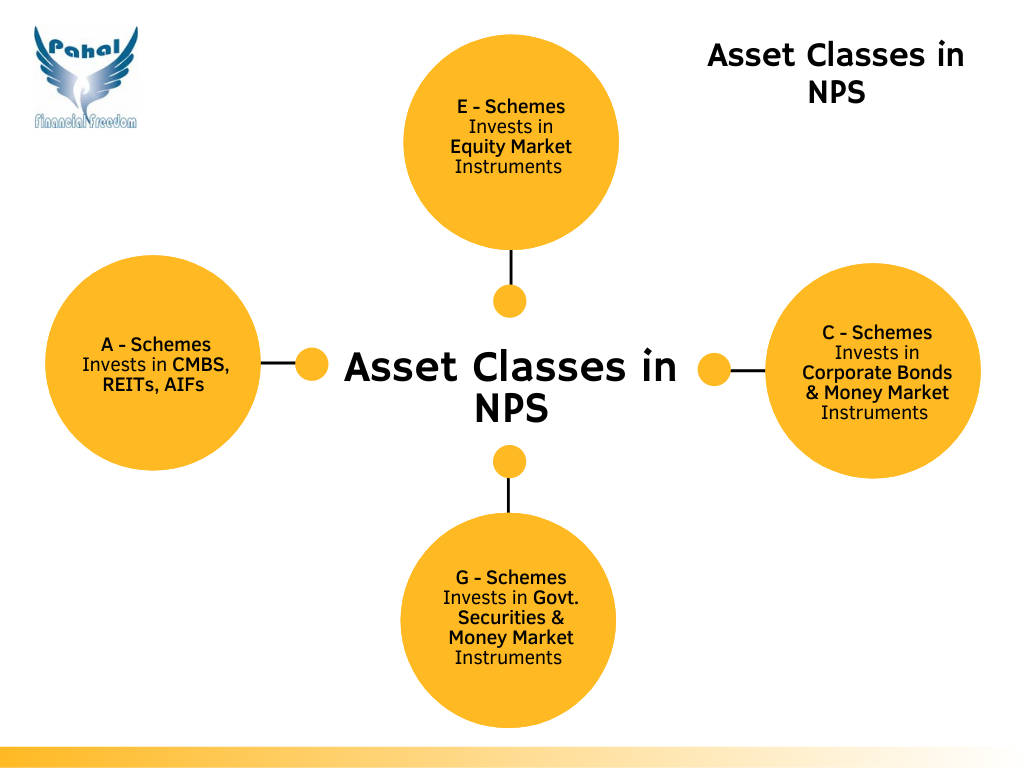

Different Asset Classes in NPS

With NPS, you can spread your investments in 4 different asset classes. This is not possible in the case of Employee Provident Fund (EPF) and Public Provident Fund (PPF)

Asset Allocation Choices in NPS

- Equities (E)– The money is invested in the stocks and other equity-related instruments of companies listed in India.

- Corporate Debt (C)– The money allocated is primarily invested in Money Market Instruments and Bonds issued by various Corporations including Infrastructure Companies, PSUs (Public Sector Units), and PFIs (Public Financial Institutions)

- Government Securities (G) – The money is invested in Money Market Instruments and Bonds issued by the State and Central Governments

- Alternative Investment Funds (A) – The money will be invested in followin instruments

- Real Estate Investment Trusts (REITs),

- Infrastructure Investment Trusts (InvITs),

- Commercial Mortgage-Backed Securities (CMBS),

- Mortgage-Backed Securities (MBS), etc.

NPS allows you to customize your NPS asset allocation as per your risk profile.

Currently, NPS offers you two options to choose the asset allocation for your NPS portfolio. Auto Choice and Auto Choice.

1. Auto Choice

This allows you to automate your NPS asset allocation. Auto Choice works on the principle that as you grow older and get closer to retirement, your focus must be on wealth preservation by minimizing the overall portfolio risk. The main purpose of It achieves this by modifying your NPS asset allocation as per your age.

Auto Choice offers some amount of flexibility. In NPS Auto Choice, you have 3 different assets allocation models known as Life Cycle Funds.

Aggressive Life Cycle Fund (LC 75):

You can take equity exposure of up to 75% till the age of 35 years in the Aggressive Life Cycle Fund.

NPS Equity allocation decreases by 4% every year. This money moves to Corporate Debt and Government Securities from age 36 years onwards.

Additional, fresh investments to NPS will be distributed across Equities, Corporate Debt, and Government Securities as per the age-based allocation specified by LC75.

If you invest in the LC75 NPS Auto Choice option, your investments across various asset classes will change like this:

LC75 offers high Equity exposure of up to 75% in your early 30s. This helps you to grow your Retirement Savings. The automatic shift of the Equity allocation portfolio towards Government Securities and Corporate Debt as you grow older. This helps to reduce the short-term volatility in your NPS account and ensures wealth preservation to secure your financial future post-retirement.

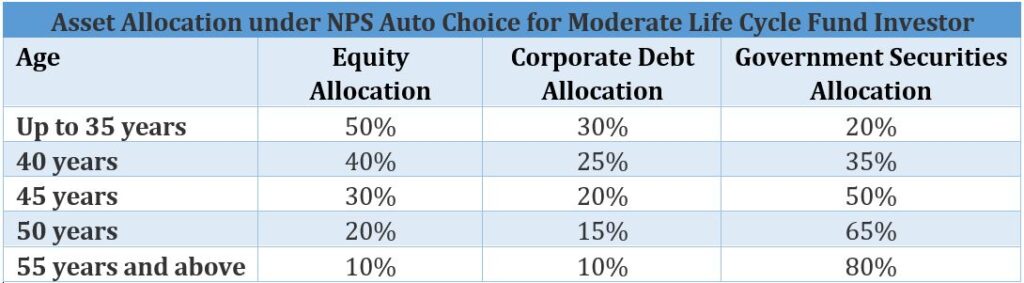

Moderate Life Cycle Fund (LC50): Moderate Life Cycle fund is also known as LC50. This is the default option under the NPS Auto Choice option. If you select the Moderate Life Cycle Fund, your maximum Equity exposure will be 50% up to the age of 35 years.

NPS asset allocation towards Equities decreases by 2% every year and that money moves to Corporate Debt and Government Securities from age 36 years onwards.

The below table shows how NPS portfolio allocation across Equities, Corporate Debt, and Government Securities will change with your age if you opt for the Moderate Life Cycle Fund:

The Moderate Life Cycle Fund aims to provide an NPS Equity allocation that offers an optimal balance between capital appreciation and wealth preservation.

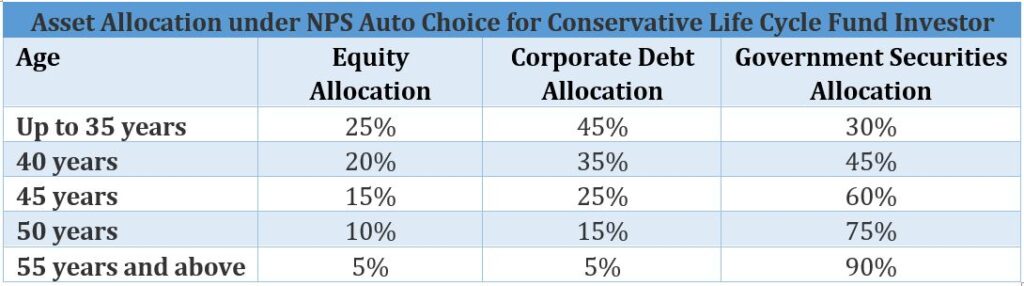

Conservative Life Cycle Fund (LC25): LC25 option is the most cautious of all the options available. If you select the Conservative Life Cycle Fund, your maximum Equity exposure will be 25% up to the age of 35 years.

NPS asset allocation towards Equities decreases by 1% every year and that money moves to Corporate Debt and Government Securities from age 36 years onwards.

The allocation across different asset classes for investors in different age groups opting for the LC25 Conservative Life Cycle Fund will be something like this:

By limiting NPS portfolio allocation towards Equities, the Conservative Life Cycle Fund focuses on wealth preservation and limits short-term portfolio volatility.

LC25 investment option is ideally suitable for low-risk appetite investors.

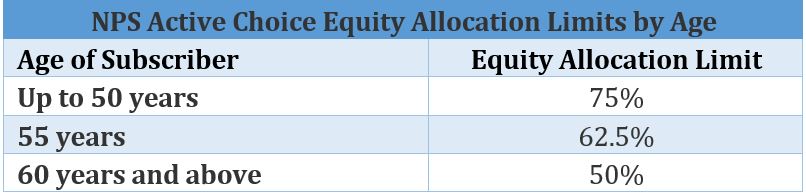

2. Active Choice

The Active Choice option of NPS offers you the highest flexibility in selecting the proportion of Equity, Corporate Debt, Government Securities, and Alternative Investment Funds in your portfolio.

There are some restrictions regarding how much you can allocate towards individual investment options:

- Maximum allocation permitted towards Alternative Investment Funds (AIFs) is 5%

- Maximum Equity exposure permitted in NPS is 75% up to the age of 50 years.

Apart from these two restrictions, there is one more condition.

NPS asset allocation towards Equities decreases by 2.5% every year. Money moves to Corporate Debt or Government Securities as per your wish.

The NPS Equity allocation limit for investors of different ages who opt for Active Choice looks like this:

You should keep in mind that these are the maximum permissible limits of Equity allocation under NPS Active Choice.

The key benefit of Active Choice is the freedom you get in choosing the NPS asset allocation that you think is most suitable to reach your investment goals.

NPS Active Choice automatically reduces your NPS portfolio’s allocation to Equities as you get closer to retirement. It increases the proportion of Debt investments to help contain the potential volatility in your portfolio.

Taxation Benefit in NPS

NPS tax benefit is available only in NPS Tier 1 Pension Account. Individuals can take tax benefits under three sections.

- Under Section 80 C (Section 80 CCD – 1):

- You can get the tax benefit of Rs. 1,50,000 under section 80 CCD – 1. NPS can be consider as one a option along with EPF , PPF, Life Insurance Policy Premium, Tax saving Mutual funds etc.

- The deduction under u/s 80CCD(1) is available for self-employed individuals to the maximum of 20% of Gross income.

- For salaried employees, the subscriber’s own contribution towards NPS is tax-deductible up to 10% of Salary (Basic + Dearness Allowance). The deduction u/s 80CCD(1) is available within the maximum limit of Rs . 1,50,000 u/s 80CCE which states that the total deduction claimed u/s 80C, 80CCC and 80CCD shall not exceed Rs . 1,50,000.

- Under Section 80 CCD (1B):

- This benefit is given to NPS Tier 1 Pension Account Holder. Under this section, one can claim deductions for investment in NPS for up to Rs. 50,000. This is over and above the Section 80C deductions.

- You can get tax benfit up to Rs. 2,00,000 under section 80 C and under Section 80 CCD 1B.

- Under Section 80 CCD (2):

- This benefit is over and above limit of 80 C and it is applicable to salaried individuals.

- A corporate subscriber is one where the employees of a corporate entity are enrolled by the employer under NPS.

- On the contribution made by the employer in NPS, one can claim a tax deduction up to 10% of salary (basic + dearness allowance). Governemnt employee claim a tax deduction up to 14% of salary.

Withdrawal Norms from NPS and its Tax Treatment

NPS is typically a retirement product. So rules are framed such that it returns in form of pension income to retirees and is not only available as a one-time corpus. Full corpus accumulated in the NPS account can not be withdrawn.

If the subscriber has joined the NPS between 18-60 years, on attaining 60 years or superannuation (as per service rules), at least 40% of the corpus is utilized for the purchase of an annuity and the remaining 60% may be withdrawn as a lump sum. Amount invested in the purchase of annuity and lump sum withdrawal are fully exempt from tax.

However, annuity income (Pension) will be subject to income tax as per the investor’s tax slab. The scheme also gives an option to defer the withdrawal up to 70 years of age.

Various other options such as deferment of annuity purchase up to 3 years, withdrawal in 10 installments, a continuation of contribution up to 70 years are also available. If Corpus is less than Rs. 2 lakhs the entire amount can be withdrawn tax-free. If the subscriber has joined the NPS between 60-65 years, the subscriber can exit after the completion of 3 years. Other provisions being largely similar.

Before attaining 60 years or superannuation, an investor in the NPS can avail of premature exit after 10 years from the date of opening the account wherein 20% of the corpus can be redeemed. 80% of the corpus will be utilized in the purchase of an annuity.

The redemption amount and amount invested in the purchase of annuity are fully exempt from tax. However, annuity income (Pension) will be subject to income tax as per the investor’s slab. In this case, if the corpus is less than or equal to Rs.1 lakh the entire amount can be withdrawn tax-free.

If the subscriber has joined the NPS between 60-65 years and wants to exit before the completion of 3 years, similar provisions as explained above would apply.

The National Pension Scheme also offers the facility of three partial withdrawals from the account opening. Partial withdrawal is allowed only in certain specified cases, for example, higher education of children, the marriage of children, for the purchase/construction of the residential house, for treatment of critical illnesses, etc.

The first partial withdrawal can be done three years after the account is opened. There should be a minimum gap of five years between two withdrawals. Each partial withdrawal should not exceed 25% of the investor’s own contribution to NPS. Partial withdrawal is tax-exempt.

In the case of the death of the investor, the nominee / legal heir can claim the corpus. Full withdrawal by the nominee / legal heir is allowed and remains tax-free. Nominee / Legal heir can opt to purchase an annuity from this accumulated wealth. The pension income would be taxed as per the nominee / legal heir’s income tax slab.

Happy Reading!!!!

Viralkumar Shah (Certified Financial Planner CM – USA)

Financial Happiness and Wellness Coach