Imagine this—you start your Systematic Investment Plan (SIP) with the goal of long-term wealth creation. But then, the stock market crashes and your portfolio turns red.

Fear kicks in. “Should I stop my SIP?”

If this thought has crossed your mind, you’re not alone. Many investors panic and pause their SIPs during market downturns. But what if I told you that SIPs work best in falling markets?

Let’s explore a real-life example that proves why staying invested through market crashes is the smartest move for long-term wealth creation.

The Dot-Com Bubble: A Market Crash That Made Investors Millions

Meet Ravi and Sameer—two investors who started their SIPs around the dot-com bubble burst, one of India’s worst stock market crashes.

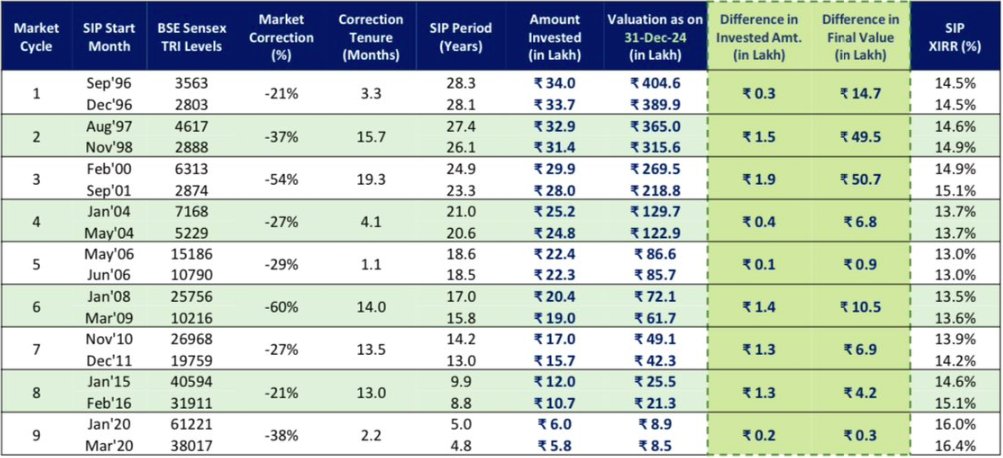

📉 February 2000: Ravi started his ₹25,000 monthly SIP, but the market soon crashed by 54%, lasting 19 brutal months. His portfolio was deep in the red.

📈 September 2001: Sameer waited for the market bottom and then started his ₹25,000 SIP.

Both continued investing till December 2024. But when they checked their portfolios, the results were shocking.

Who Made More Money?

Investor

SIP Start Date

Total Invested

Final Portfolio Value (Dec 2024)

🟥 Ravi (Started at the Top)

Feb 2000

₹74.75 Lakh

₹6.70 Crore

🟩 Sameer (Started at the Bottom)

Sep 2001

₹70 Lakh

₹5.50 Crore

💡 Surprised? Ravi made ₹1.2 Crore MORE than Sameer, despite investing just ₹4.75 Lakh extra! But how?

Why Did Starting at the Top Work Better?

Most people believe that investing at market peaks is risky, but data tells a different story.

✅ SIPs Buy More Units When Markets Fall

When the market crashes, your SIP automatically buys more mutual fund units at lower prices. Over time, these extra units generate higher returns.

✅ Compounding Works Best Over the Long Term

By staying invested for 25 years, Ravi’s returns compounded significantly more than Sameer’s.

✅ Timing the Market is a Myth

Even if you start investing at the worst possible time, long-term investing ensures you benefit from market recovery and growth.

A study by WhiteOak CapitalMutual Fund shows that in the last 28 years, every major market correction has rewarded patient SIP investors.

What Should You Do When the Market Crashes?

The next time the stock market crashes, ask yourself these two important questions:

🔹 Should I stop my SIP? No! This is when SIPs work the best. Lower prices mean you accumulate more units, boosting future returns.

🔹 Am I a long-term investor? If you’re investing for financial freedom in 20-25 years, short-term market crashes should not worry you. Patience is the key.

Final Takeaway: The Best SIP Strategy is to Stay Invested

Here’s the biggest lesson from Ravi’s story:

If you can’t time the market, don’t try. Just stay invested.

Market crashes are not the enemy—they are opportunities to build wealth faster.

So, the next time you see your portfolio in red, don’t panic—celebrate! History has shown that SIP investors who stay invested always come out wealthier in the end. 🚀

Want to Build Wealth Without Stress?

Start your SIP today and stay invested for the long term. Your future self will thank you! 😊

Happy Reading & Happy Investing!!!

Viralkumar Shah (Certified Financial Planner CM – USA)

Author – Financial Planning Sahi Hai! –Keep Your Life Organized

The power of compounding can greatly benefit those looking to build wealth through investing. It is essential to understand the advantages of compounding and select the appropriate investment vehicle. While direct stock investing may be tempting, mutual funds offer specific benefits that can accelerate your investment growth. This blog will discuss why mutual funds excel over direct stock investing in harnessing the power of compounding.

When it comes to compounding, mutual funds, and direct stock investing have different levels. With direct stock investing, your investments grow over time as you earn returns from dividends and capital gains. This is called basic compounding or level 1 compounding, where you earn returns on both your initial investment and the accumulated returns. Let’s take an example to illustrate this: Suppose you invest Rs. 1,00,000 in a stock. After one year, it grows by 10% and becomes Rs. 1,10,000. In the second year, it grows by another 10%, resulting in Rs. 1,21,000.

Mutual funds harness the power of pooling money from numerous investors, allowing you to tap into the advantages of compounding on a grander scale. Rather than going it alone, you join forces with others, contributing your funds to a collective investment vehicle. This approach opens doors to larger and more diversified opportunities that an individual investor might find challenging to access independently. With professional expertise at the helm and the economies of scale that come with pooled resources, mutual funds provide a strategic avenue for growing your wealth through compounding over time.

Over time, the fund increases in value by reinvesting its earnings, such as dividends and capital gains, into more shares. This helps to boost the compounding effect.

Mutual funds provide the opportunity to access better investments and lower transaction costs, which can potentially lead to higher returns. It allows people to pool their money and benefit from combined resources for increased returns.

As a result, there are higher returns due to economies of scale, diversification, and professional management, which enhance growth potential for all involved as opposed to investing directly in individual stocks.

Happy Reading & Happy Investing!!!

Viralkumar Shah (Certified Financial Planner CM – USA, Financial Happiness & Wellness Coach)

Author – Financial Planning Sahi Hai! –Keep Your Life Organized

“Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn’t, pays it” – Albert Einstein

Initially, this statement may appear to be an overstatement, but the mathematical calculations supporting it prove otherwise. Allow me to present a fascinating illustration: Imagine you possess a sum of Rs 5 crore at the age of 50 and your investment is growing at 12% return then as per Rule of 72, your money will double every 6 years.

It is possible to increase your wealth to 10 crores in six years from now. You can set aside 5 crores of this amount to cover all of your living expenses. Every six years, the remaining 5 crores will double in value.

When you turn 62 years old, your wealth will total 10 crores. As you progress to 68, it will double to 20 crores. Moving forward to 74, it will grow to 40 crores. Upon reaching 80, your wealth will soar to 80 crores. By the time you turn 86, it will reach an impressive 160 crores. This extraordinary financial growth only requires an additional 5 crores to secure the future for all your generations to come.

So, what will happen with the surplus? You can either use it to benefit society, or the government will disperse it later. This demonstrates the power of compounding, a concept that is sometimes underestimated.

Key Takeaways

A. Ensuring Financial Stability: Through strategic management and wise investments of a significant starting amount, people can ensure their financial stability and create a comfortable lifestyle for both themselves and their loved ones.

B. Creating a Meaningful Impact: Harnessing surplus wealth to bring about a positive change in society allows individuals to make a profound and enduring impact that surpasses mere monetary wealth. By doing so, they contribute to the progress of future generations and address the societal requirements.

C. Recognizing the Power of Compound Growth: Understanding the principle of compounding emphasizes the importance of strategic long-term financial planning and prudent investment strategies, showcasing the significant opportunity for wealth accumulation that arises from consistent saving and investing.

Happy Reading & Happy Investing!!!

Viralkumar Shah (Certified Financial Planner CM – USA, Financial Happiness & Wellness Coach)

Author – Financial Planning Sahi Hai! –Keep Your Life Organized

With the market reaching new heights, many investors have questions. Have the Market reached the upper limit? Can we invest more even now?

The possibility that markets may now decline also crosses one’s mind. I do not see any evidence to support this. And yes, it is also true that it is unclear whether the market will increase or decrease soon. We only speculate based on our own biases; nobody knows. In the short term, markets reflect market sentiment, but in the long run, they reflect the state and health of the economy.

Imagine the Economy was a car 🚗 which had a speed of 100 km per hour with a 150 Horse Power Engine. The speed has now increased to 150 km/h, but this does not mean that the speed has reached its maximum – this is an important point to understand.

The reason for this is that the car’s power has increased from 150 to 200 horsepower. This means the car has the potential and energy to accelerate even further and reach much higher speeds.

The Market Index Level is the speed here, and the Horse Power is the Market P/E.

All I can say is that, despite the fact that the markets are reaching new heights and may be more expensive than the historical average valuation, the current market is still less expensive than the pre-covid markets.

Observe the graph or table below:

Month

Sensex

P/E Value

Jun-19

39,395

28.27

Jun-23

64,719

23.33

Rise / Fall

64.3%

-17.5%

Note: Trailing Valuation

The valuation is still relatively less expensive than pre-covid levels, despite new highs.

Invest wisely.

Courtacy of the Article: Krishan Sharma and Dharmendra Satapathy

Happy Reading & Happy Investing!!!

Viralkumar Shah (Certified Financial Planner CM – USA)

Author – Financial Planning Sahi Hai! –Keep Your Life Organized

Before learning the secret to leading a quality life, let’s first understand financial freedom. Financial freedom means having enough money to live the life you want. It means that one can buy whatever they want without worrying about where the money will come from.

Financial freedom is determined by factors such as returns, inflation, initial corpus, and withdrawal amount. However, the last component Withdrawal amount / Life Style Cost is the most important out of all of them.

Lifestyle costs are compounded by the inflation rate. As a result, a higher standard of living will attract higher lifestyle inflation. This would enlarge the Freedom Corpus and make it difficult to create it on time.

“If standard of living is your number one objective, quality of life almost never improves. But if quality of life is your number one objective, standard of living invariably improves.” – Zig Zaglar

Courtesy: Quantum Thinker

The game of Financial Freedom is getting there early.Therefore, adopting a simple lifestyle becomes the most crucial aspect of achieving financial freedom as soon as possible. As a result, the lower-middle-income classes are well-positioned to achieve financial independence if they are guided. This is due to the fact that they live well below their means and find happiness in the simple things in life.

Simple living is the best way to achieve financial freedom. Once you have achieved financial freedom, it is easier to take risks, find success, and gradually and steadily improve the quality of your lifestyle.

Therefore, “Quality of Lifestyle enhancements in a sustainable manner” is the new phrase. There is no point in living an expensive lifestyle that could end at any time.

Financial Planning Solutions can transform lives and bring true happiness. If you quality of life then you can reach out to us.

Happy Reading.

Viralkumar Shah (Certified Financial Planner CM – USA)

Author – Financial Planning Sahi Hai! –Keep Your Life Organized

Pay higher taxes on your debt, Gold & International Mutual funds now.

What has changed?

Now you have to pay Tax as per your slab rate irrespective of your holding period on the gain from your Debt, Gold, International, FOFs Mutual Funds (any MF which will have 35% or less AUM in domestic equity).

What is the Current provision?

Currently, if you hold these funds for over 3 years, it is considered a Long-term capital gain and you have to pay 20% tax after indexation. Holding less than 3 years, it’s a short-term capital gain, and it’s taxed as per your slab rate.

When this is announced?

This was not there in the original budget document. This has been announced on 22.03.2023 as an amendment to Finance Bill 2023 (Budget 2023).

When this will apply from?

Applicable from 1st April 2023.

So, whatever amount invested till now and investments to be done before 31.03.2023 continue to get long-term capital gain tax rate of 20% and indexation benefits.

Categories after this amendment in Mutual fundsfor Tax Purposes:

So, now there will be 3 categories of funds for tax purposes:

1. Funds holding 65% or more of Indian equity:

LTCG – 10% LTCG above 1 lakh if hold for more than one year

STCG at 15% (No change)

2. Funds holding over 35% but less than 65% of Indian equity:

LTCG – Indexation benefit and 20% tax rate

STCG – Tax as per slab rate

3. Funds holding 35% or less Indian equity:

STCG will be applicable and taxed at a Slab rate for the individual.

Final Comments:

I believe this is a terrible move from the government. Debt and Gold MFs require encouragement considering the need for this asset class in one’s portfolio as part of asset allocation, debt has already have low penetration and this move of the government will affect it badly.

Happy Reading.

Viralkumar Shah (Certified Financial Planner CM – USA)

Author – Financial Planning Sahi Hai! –Keep Your Life Organized

When you think about your personality traits, what words come to mind? Impulsive? Confident? Organized? Consider how you make investment decisions. Would the same words be appropriate?

Certain psychological characteristics can have an impact on your investment decisions, often at the expense of logic. As a result, investment returns may fall short of your expectations.

Consider the following characteristics. Could any of these be hindering your success with investments?

Comparators, Complainers, and Controllers are the three personality types that might harm an investor’s investment journey and hinder them from having a successful investing experience.

Comparators always look dissatisfied with their investment returns and continually compare them to those of their peers, co-workers, and acquaintances. The “uski kameez, mere kameez, se safed kaise” syndrome is the cause of this. When they are ahead, they simply do not care, but when they are slipping behind, they always complain.

Complainers are investors who are perpetually complaining about the markets, the economy, their adviser, their luck, and, of course, their returns. Such people will never achieve their primary goal of attaining happiness.

Controllers are investors who believe they can exert influence over the ecosystem. They continue to seek formulas, theories, and hypotheses in the hope of outperforming everyone. They also have a bad habit of hiring an adviser but not giving him any authority, instead relying on him to advise him. They appear to know more about investing than even Warren Buffett.

If you have any of the three personality types listed above, you need a professional adviser more than anyone else, because your personality type will be the most difficult obstacle for your investment portfolio.

Happy Reading!!!

Viralkumar Shah (Certified Financial Planner CM – USA)

The rich don’t work for money. The poor and the middle class work for money. The rich have money to work for them. – Robert Kiyosaki

When you work for money, youpay a 30% tax; when money works for you, you pay only a 10% tax. You have a boss to please when you work for money; when money works for you, you are the boss to please. When you work for a living, your pay is a mystery. But when money works for you, it’s a beautiful story.

When you work for money, you must apply for holiday leave; when your money works for you, your life is a vacation. When you work for money, your time is not your time; when your money works for you, you are the lord of your time.

Source: Slideshare

When you work for money, you must wear various masks to survive. You can be yourself when your money works for you. When you work for money, you become a puppet in the political whirlpool; when money works for you, you remain above politics.

You are in the rat race when you work for money. You can casually walk at your own pace when money works for you. When you work for money, your EMI is like a sword that hangs over you; when money works for you, your SIP is like a shield that protects you from every adversary.

You are full of jealousy when you work for money. Nobody can envy you when money works for you. When you work for money, Monday morning blues set in; when money works for you, you do not know what day it is.

When you work for money, everything around you is insecure; when money works for you, everything around you is very secure. You crave a little family life when you work for money; when money works for you, your family becomes your entire life.

When you work for money, your vision is leadership, and your mission is market share; when money works for you, your vision is problem-solving, and your mission is team building. When you work for money, your hunger grows; when money works for you, you consider world hunger.

You want a jet-like speed when you work for money; when money works for you, you can slow down and see, smell, and savor the surrounding beauty. You hope for compounding when you work for money; when money works for you, you experience compounding.

When you work for money, you see wealth in happiness; when money works for you, you see happiness in wealth. If you want money to work for you, create a financial freedom road map.

Happy Reading!!!

Viralkumar Shah (Certified Financial Planner CM – USA)

National Pension System (NPS) is a voluntary, defined contribution retirement savings system. The scheme was introduced in Jan 2014 for the new government employees. NPS is mandatory for all central government employees along with some State government employees who’ve joined after Jan 2004. All can invest in NPS from May 2009.

The main objective of the system is to develop a habit of saving for retirement.

The scheme falls under the jurisdiction of the Pension Fund Regulatory and Development Authority (PFRDA). The aim of NPS is to provide monetary benefits in the form of a pension after an individual reaches retirement.

Eligibility Criteria

Entry age 18 years to 70 years.

Person must be Resident Indian, Non-Resident Indian (NRI), or Overseas Citizen of India (OCI).

Provide valid KYC documents like PAN Card, Address Proof and Aadhar Card etc along with NPS application.

If you meet all the above criteria, you are eligible to open both the NPS Tier 1 Pension Account & NPS Tier 2 Investment Account.

Unicque Selling Proposition of NPS (USP)

NPS is a low-cost product. NPS Tier 1 Pension Account is also providing tax benefits. You are free to choose various asset classes like Equity, Government Bond, Corporate Bond, and Alternate Asset class for investment. You can decide the proportion of asset class as per your risk-taking ability.

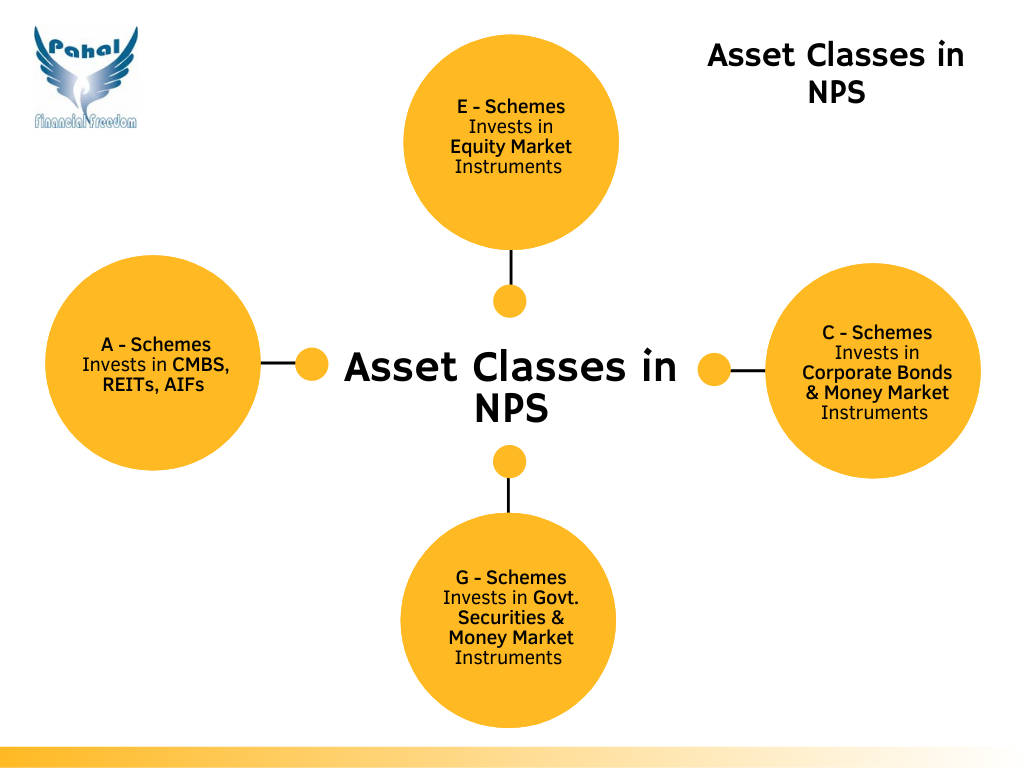

Different Asset Classes in NPS

With NPS, you can spread your investments in 4 different asset classes. This is not possible in the case of Employee Provident Fund (EPF) and Public Provident Fund (PPF)

Asset Allocation Choices in NPS

Equities (E)– The money is invested in the stocks and other equity-related instruments of companies listed in India.

Corporate Debt (C)– The money allocated is primarily invested in Money Market Instruments and Bonds issued by various Corporations including Infrastructure Companies, PSUs (Public Sector Units), and PFIs (Public Financial Institutions)

Government Securities (G) – The money is invested in Money Market Instruments and Bonds issued by the State and Central Governments

Alternative Investment Funds (A) – The money will be invested in followin instruments

Real Estate Investment Trusts (REITs),

Infrastructure Investment Trusts (InvITs),

Commercial Mortgage-Backed Securities (CMBS),

Mortgage-Backed Securities (MBS), etc.

NPS allows you to customize your NPS asset allocation as per your risk profile.

Currently, NPS offers you two options to choose the asset allocation for your NPS portfolio. Auto Choice and Auto Choice.

1. Auto Choice

This allows you to automate your NPS asset allocation. Auto Choice works on the principle that as you grow older and get closer to retirement, your focus must be on wealth preservation by minimizing the overall portfolio risk. The main purpose of It achieves this by modifying your NPS asset allocation as per your age.

Auto Choice offers some amount of flexibility. In NPS Auto Choice, you have 3 different assets allocation models known as Life Cycle Funds.

Aggressive Life Cycle Fund (LC 75):

You can take equity exposure of up to 75% till the age of 35 years in the Aggressive Life Cycle Fund.

NPS Equity allocation decreases by 4% every year. This money moves to Corporate Debt and Government Securities from age 36 years onwards.

Additional, fresh investments to NPS will be distributed across Equities, Corporate Debt, and Government Securities as per the age-based allocation specified by LC75.

If you invest in the LC75 NPS Auto Choice option, your investments across various asset classes will change like this:

LC75 offers high Equity exposure of up to 75% in your early 30s. This helps you to grow your Retirement Savings. The automatic shift of the Equity allocation portfolio towards Government Securities and Corporate Debt as you grow older. This helps to reduce the short-term volatility in your NPS account and ensures wealth preservation to secure your financial future post-retirement.

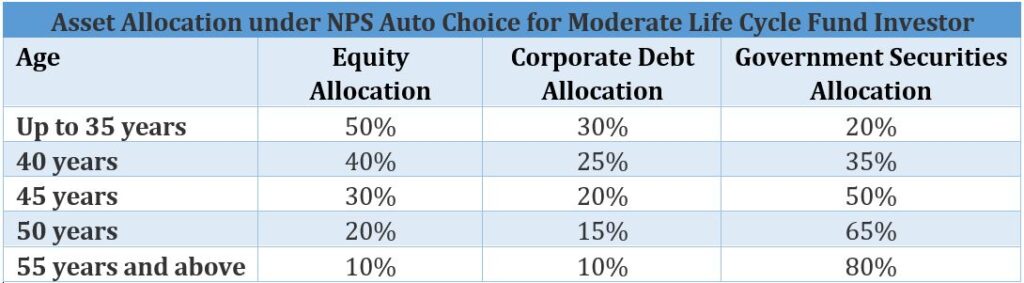

Moderate Life Cycle Fund (LC50): Moderate Life Cycle fund is also known as LC50. This is the default option under the NPS Auto Choice option. If you select the Moderate Life Cycle Fund, your maximum Equity exposure will be 50% up to the age of 35 years.

NPS asset allocation towards Equities decreases by 2% every year and that money moves to Corporate Debt and Government Securities from age 36 years onwards.

The below table shows how NPS portfolio allocation across Equities, Corporate Debt, and Government Securities will change with your age if you opt for the Moderate Life Cycle Fund:

The Moderate Life Cycle Fund aims to provide an NPS Equity allocation that offers an optimal balance between capital appreciation and wealth preservation.

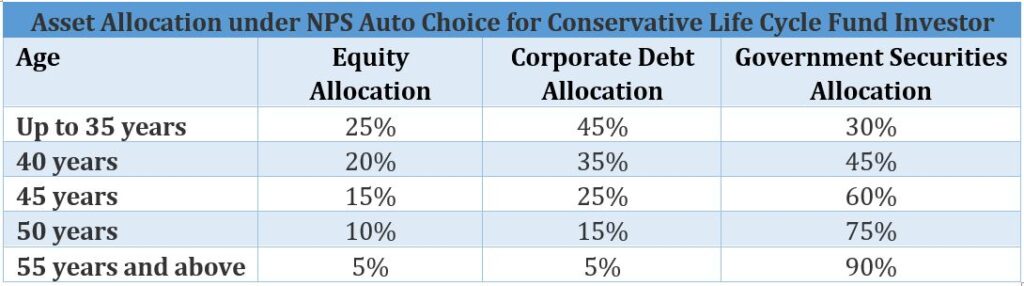

Conservative Life Cycle Fund (LC25): LC25 option is the most cautious of all the options available. If you select the Conservative Life Cycle Fund, your maximum Equity exposure will be 25% up to the age of 35 years.

NPS asset allocation towards Equities decreases by 1% every year and that money moves to Corporate Debt and Government Securities from age 36 years onwards.

The allocation across different asset classes for investors in different age groups opting for the LC25 Conservative Life Cycle Fund will be something like this:

By limiting NPS portfolio allocation towards Equities, the Conservative Life Cycle Fund focuses on wealth preservation and limits short-term portfolio volatility.

LC25 investment option is ideally suitable for low-risk appetite investors.

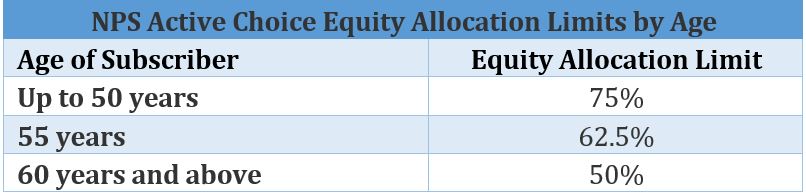

2. Active Choice

The Active Choice option of NPS offers you the highest flexibility in selecting the proportion of Equity, Corporate Debt, Government Securities, and Alternative Investment Funds in your portfolio.

There are some restrictions regarding how much you can allocate towards individual investment options:

Maximum allocation permitted towards Alternative Investment Funds (AIFs) is 5%

Maximum Equity exposure permitted in NPS is 75% up to the age of 50 years.

Apart from these two restrictions, there is one more condition.

NPS asset allocation towards Equities decreases by 2.5% every year. Money moves to Corporate Debt or Government Securities as per your wish.

The NPS Equity allocation limit for investors of different ages who opt for Active Choice looks like this:

You should keep in mind that these are the maximum permissible limits of Equity allocation under NPS Active Choice.

The key benefit of Active Choice is the freedom you get in choosing the NPS asset allocation that you think is most suitable to reach your investment goals.

NPS Active Choice automatically reduces your NPS portfolio’s allocation to Equities as you get closer to retirement. It increases the proportion of Debt investments to help contain the potential volatility in your portfolio.

Taxation Benefit in NPS

NPS tax benefit is available only in NPS Tier 1 Pension Account. Individuals can take tax benefits under three sections.

Under Section 80 C (Section 80 CCD – 1):

You can get the tax benefit of Rs. 1,50,000 under section 80 CCD – 1. NPS can be consider as one a option along with EPF , PPF, Life Insurance Policy Premium, Tax saving Mutual funds etc.

The deduction under u/s 80CCD(1) is available for self-employed individuals to the maximum of 20% of Gross income.

For salaried employees, the subscriber’s own contribution towards NPS is tax-deductible up to 10% of Salary (Basic + Dearness Allowance). The deduction u/s 80CCD(1) is available within the maximum limit of Rs . 1,50,000 u/s 80CCE which states that the total deduction claimed u/s 80C, 80CCC and 80CCD shall not exceed Rs . 1,50,000.

Under Section 80 CCD (1B):

This benefit is given to NPS Tier 1 Pension Account Holder. Under this section, one can claim deductions for investment in NPS for up to Rs. 50,000. This is over and above the Section 80C deductions.

You can get tax benfit up to Rs. 2,00,000 under section 80 C and under Section 80 CCD 1B.

Under Section 80 CCD (2):

This benefit is over and above limit of 80 C and it is applicable to salaried individuals.

A corporate subscriber is one where the employees of a corporate entity are enrolled by the employer under NPS.

On the contribution made by the employer in NPS, one can claim a tax deduction up to 10% of salary (basic + dearness allowance). Governemnt employee claim a tax deduction up to 14% of salary.

Withdrawal Norms from NPS and its Tax Treatment

NPS is typically a retirement product. So rules are framed such that it returns in form of pension income to retirees and is not only available as a one-time corpus. Full corpus accumulated in the NPS account can not be withdrawn.

If the subscriber has joined the NPS between 18-60 years, on attaining 60 years or superannuation (as per service rules), at least 40% of the corpus is utilized for the purchase of an annuity and the remaining 60% may be withdrawn as a lump sum. Amount invested in the purchase of annuity and lump sum withdrawal are fully exempt from tax.

However, annuity income (Pension) will be subject to income tax as per the investor’s tax slab. The scheme also gives an option to defer the withdrawal up to 70 years of age.

Various other options such as deferment of annuity purchase up to 3 years, withdrawal in 10 installments, a continuation of contribution up to 70 years are also available. If Corpus is less than Rs. 2 lakhs the entire amount can be withdrawn tax-free. If the subscriber has joined the NPS between 60-65 years, the subscriber can exit after the completion of 3 years. Other provisions being largely similar.

Before attaining 60 years or superannuation, an investor in the NPS can avail of premature exit after 10 years from the date of opening the account wherein 20% of the corpus can be redeemed. 80% of the corpus will be utilized in the purchase of an annuity.

The redemption amount and amount invested in the purchase of annuity are fully exempt from tax. However, annuity income (Pension) will be subject to income tax as per the investor’s slab. In this case, if the corpus is less than or equal to Rs.1 lakh the entire amount can be withdrawn tax-free.

If the subscriber has joined the NPS between 60-65 years and wants to exit before the completion of 3 years, similar provisions as explained above would apply.

The National Pension Scheme also offers the facility of three partial withdrawals from the account opening. Partial withdrawal is allowed only in certain specified cases, for example, higher education of children, the marriage of children, for the purchase/construction of the residential house, for treatment of critical illnesses, etc.

The first partial withdrawal can be done three years after the account is opened. There should be a minimum gap of five years between two withdrawals. Each partial withdrawal should not exceed 25% of the investor’s own contribution to NPS. Partial withdrawal is tax-exempt.

In the case of the death of the investor, the nominee / legal heir can claim the corpus. Full withdrawal by the nominee / legal heir is allowed and remains tax-free. Nominee / Legal heir can opt to purchase an annuity from this accumulated wealth. The pension income would be taxed as per the nominee / legal heir’s income tax slab.

Happy Reading!!!!

Viralkumar Shah (Certified Financial Planner CM – USA)